Jewelry Loans: Borrow Against Fine and Designer Pieces

A diamond engagement ring, a Cartier bracelet, a Van Cleef & Arpels necklace — these are not just beautiful objects. They are assets with real, documented market value. And when you need liquidity, they can work for you without ever leaving your ownership permanently.

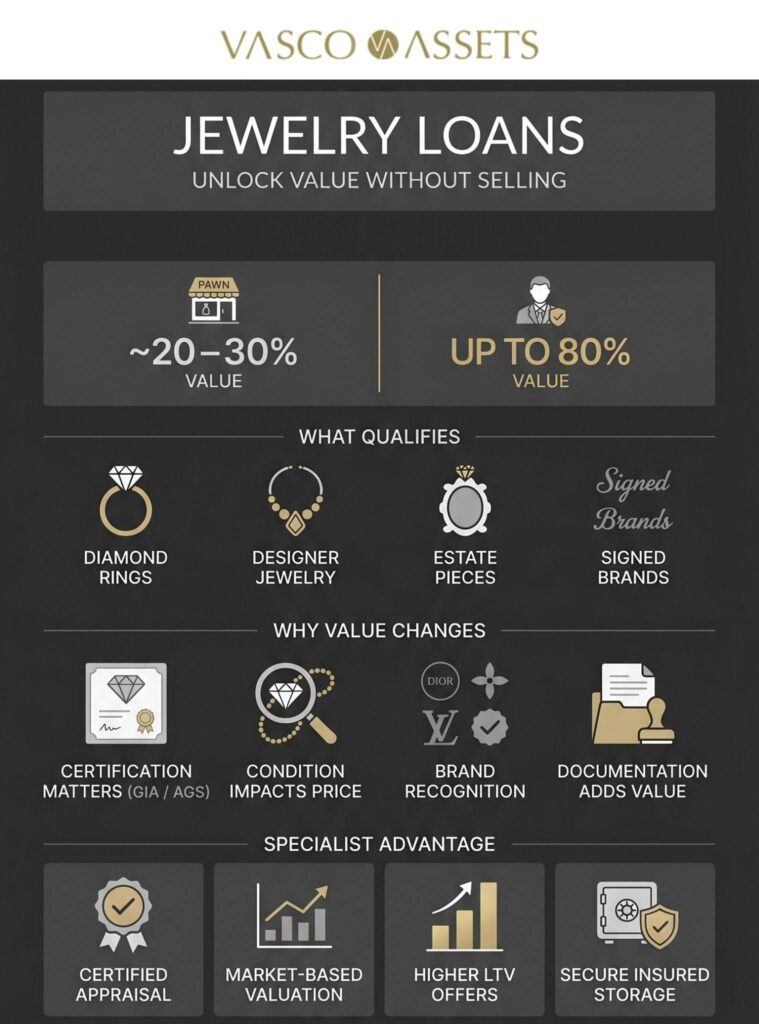

Jewelry loans allow you to borrow against the value of fine and designer pieces quickly, discreetly, and without a credit check. Vasco Assets is a California-based specialist lender that offers collateral loans against jewelry, diamonds, watches, gold, and other luxury assets — providing loan values up to 80% of assessed market worth, with funds available in as little as 24 hours.

What Is a Jewelry Loan?

Secured Lending Without the Bank

A jewelry loan is an asset-backed loan in which your piece serves as collateral instead of your credit profile. The lender appraises the item, makes a loan offer based on its current market value, and holds it securely until the loan is repaid in full. There is no income verification, no credit inquiry, and no drawn-out approval process.

How It Works at Vasco Assets

At Vasco Assets, every loan begins with a complimentary valuation. After a thorough physical inspection at Vasco’s Newport Beach headquarters, a loan offer is made and, once agreed upon, funds are issued promptly. Loan terms run 30 to 120 days with extensions available, and every piece is insured by Lloyd’s and Partners of London for twice the loan amount while in Vasco’s care.

What Types of Jewelry Qualify?

Fine Jewelry and Estate Pieces

The strongest candidates for jewelry loans are pieces that combine intrinsic material value with recognized craftsmanship or provenance. Diamond solitaire rings, multi-stone engagement rings, sapphire and emerald suites, and high-karat gold pieces all qualify. Estate jewelry with documented history or signed pieces from recognized ateliers can command particularly strong appraisals.

Designer and Signed Jewelry

Signed pieces from globally recognized maisons carry significant collateral value beyond their material components. Cartier, Van Cleef & Arpels, Bulgari, Tiffany & Co., Harry Winston, and David Yurman are among the brands whose secondary market depth gives Vasco Assets the confidence to offer strong loan-to-value ratios. Original boxes, receipts, and certificates of authenticity all support a higher loan offer.

The 7 Things That Can Reduce Your Jewelry Loan Offer

Why Two Similar Pieces Can Receive Very Different Offers

Most borrowers assume their jewelry’s retail or replacement value is what determines a loan offer. In practice, collateral lenders focus far more on liquidity, verifiability, and resale certainty. When any of those weaken, the loan-to-value ratio typically drops — sometimes significantly — which is why preparation and documentation often matter as much as the jewelry itself.

Missing Certification and Physical Condition

One of the most common value reducers is missing diamond certification. Without independent grading from institutions like the Gemological Institute of America (GIA), lenders face higher uncertainty in assessing cut, color, clarity, and carat weight — which directly impacts pricing confidence. Physical condition issues such as broken clasps, worn prongs, or damaged settings also lower offers, because they introduce repair costs and resale delays. Even small structural defects can meaningfully reduce marketability.

Personalization, Missing Provenance, and Design

Heavy personalization or engraving reduces the pool of potential secondary buyers, narrowing liquidity. Missing original boxes, receipts, or certificates similarly weakens provenance — an increasingly important factor in luxury resale markets, as reinforced by the FTC’s Jewelry Guides, which emphasize transparent and accurate representation of jewelry characteristics. Outdated or highly customized designs may also underperform compared to classic, widely traded styles simply because secondary market demand is thinner.

Unverified Gemstones and Weak Secondary Market Demand

Unverified gemstones — where a lack of documentation forces lenders to discount value due to appraisal uncertainty — are another major issue. Finally, even high-quality pieces can receive suppressed offers if comparable resale data is limited or volatile. It is important to understand that jewelry collateral lending is less about what you originally paid and more about what can be reliably resold. The IRS reinforces this distinction: tax treatment for collectibles is based on realized market value, not purchase price — a gap that can be wider than many owners expect.

How Lenders Value Jewelry

What Vasco’s Experts Evaluate

A specialist appraisal from Vasco Assets goes well beyond weighing the metal. Appraisers examine the quality and certification status of center and accent stones, assess the craftsmanship and condition of the setting, verify brand attribution where applicable, and cross-reference current secondary market data for comparable pieces. This comprehensive approach is what separates a specialist lender from a generalist pawn shop that may only offer 20–30 cents on the dollar.

Why Specialist Knowledge Changes the Outcome

A diamond solitaire appraised by someone unfamiliar with the nuances of stone grading may be undervalued by thousands of dollars. A signed Bulgari serpenti bracelet assessed without knowledge of the current collector market may receive a fraction of its true worth. Vasco Assets employs certified professionals with active knowledge of the fine jewelry secondary market, ensuring that every appraisal reflects what the piece is actually worth — not what a generalist guesses it might fetch.

Should You Borrow Against Your Jewelry or Sell It?

When a Loan Makes More Sense

Borrowing makes the most sense when your need for capital is temporary and you intend to keep the piece. If you are bridging a short-term cash-flow gap, funding a business opportunity, or covering a time-sensitive expense, a jewelry loan lets you access liquidity while retaining ownership of an heirloom or investment piece. For collectors or those with sentimental attachments, this distinction matters enormously.

When Selling Is the Right Choice

Selling may be appropriate when you no longer wear the piece, it no longer fits your collection, or your need for capital is long-term. If you do sell, be aware of the tax implications: the IRS confirms that gains on collectibles — which can include fine jewelry — may be subject to a maximum federal capital gains rate of 28%. For those considering a securities-backed alternative, the Financial Industry Regulatory Authority (FINRA) cautions that these facilities carry risks including potential forced liquidation. The clearest question to ask yourself is whether you want temporary liquidity or a permanent exit from the asset.

You Built the Collection. Now Let It Work for You.

Your Jewelry Is More Than an Accessory

Fine and designer jewelry represents decades of craftsmanship, careful acquisition, and real financial value. A jewelry loan from Vasco Assets allows you to activate that value without selling, without credit exposure, and without delay. Your piece is secured, insured, and waiting for you when the loan is repaid.

Take the First Step

Whether you own a single heirloom diamond or a curated collection of signed pieces, there is capital in your jewelry box — and Vasco has the expertise to unlock it. Request your complimentary valuation at vascoassets.com and find out exactly what your jewelry can do for you.

FAQs

1. What types of jewelry can I borrow against?

Vasco Assets accepts fine jewelry, diamond rings and suites, signed designer pieces from maisons such as Cartier, Van Cleef & Arpels, Bulgari, Tiffany & Co., and Harry Winston, as well as estate jewelry, loose diamonds, and high-karat gold pieces. A complimentary valuation will confirm what your specific piece qualifies for.

2. What are the most common things that reduce a jewelry loan offer?

The seven main factors are: missing diamond certification, physical damage or worn settings, heavy personalization or engraving, missing original boxes and documentation, outdated or highly customized designs, unverified gemstones, and weak secondary market demand. Addressing as many of these as possible before your appraisal — particularly sourcing a GIA certificate and gathering original paperwork — can meaningfully increase your loan offer.

3. Does my jewelry need to be certified or appraised beforehand?

No prior appraisal is needed — Vasco Assets provides complimentary valuations. However, existing certification documents such as a GIA or AGS grading report for diamonds, along with original boxes, receipts, and authenticity certificates, can meaningfully increase the loan offer you receive.

4. How much can I borrow against my jewelry?

Loan amounts are based on current market value. Vasco Assets can advance up to 80% of assessed value — significantly more than most pawn shops or generalist lenders. The strength of your offer depends on the piece’s liquidity, brand, documentation, condition, and the stability of its market value.

5. How is my jewelry protected during the loan?

All pieces are stored in secure, monitored vaults at Vasco’s Newport Beach headquarters and insured by Lloyd’s and Partners of London for twice the loan amount. Your jewelry is fully protected and returned in the same condition upon repayment of the principal and fees.

6. What are the loan terms and rates?

Loan terms run 30, 60, 90, or 120 days, with extensions available on request. Interest rates range from 2% to 10%, averaging around 5%, and are set in compliance with California’s Department of Justice regulations. The minimum loan amount is $2,500.

7. Can I borrow against jewelry and other assets at the same time?

Yes. Vasco Assets is experienced in portfolio-level lending and can evaluate multiple items across categories simultaneously — fine jewelry, loose diamonds, luxury watches, and gold, for example. A combined appraisal may allow you to access a larger loan against the total value of your holdings.