Luxury Pawn Shop Alternative: Loans on Watches and Jewelry

You own a Rolex. A diamond ring. A signed Cartier bracelet. You need capital — and you’ve considered walking into a pawn shop. Before you do, it is worth understanding exactly what a pawn shop is likely to offer you, and what a specialist lender can offer instead.

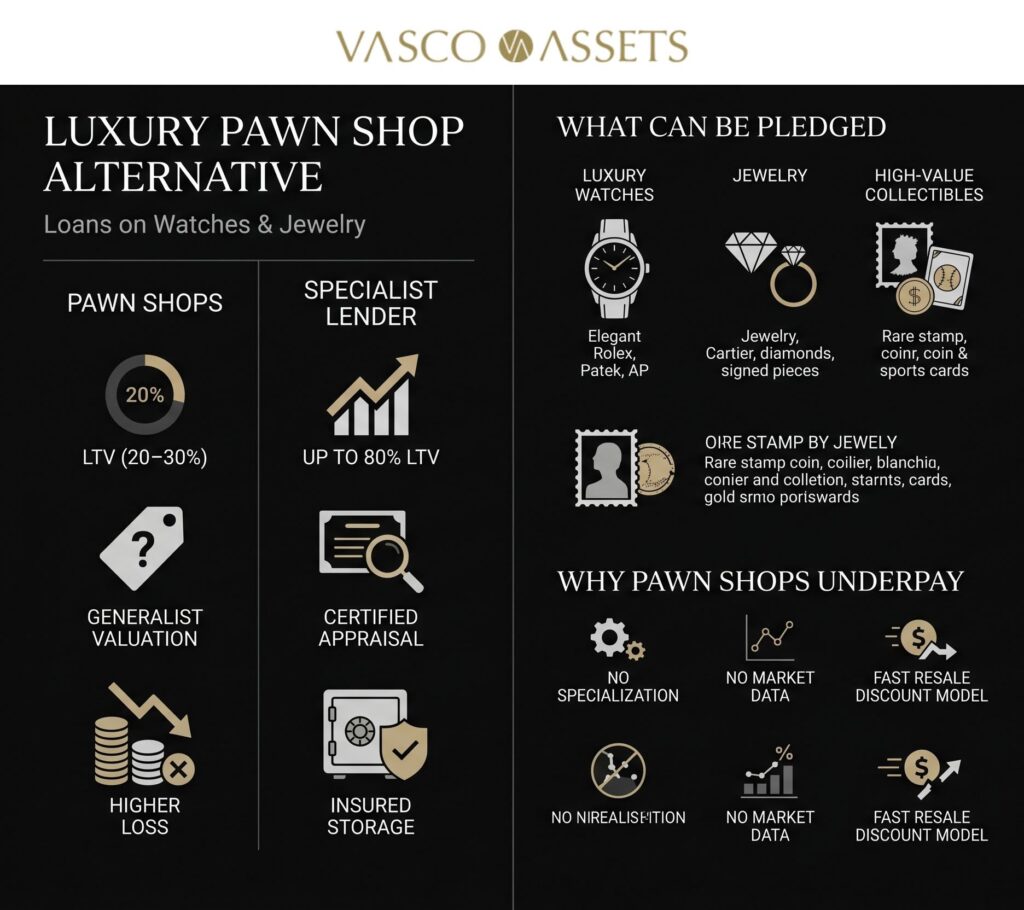

The difference is not marginal. It is the difference between 20 cents on the dollar and up to 80%. Vasco Assets is a California-based luxury asset lender that provides collateral loans against fine watches, jewelry, diamonds, and other high-value assets — with certified appraisals, insured storage, and no credit check required.

What a Traditional Pawn Shop Actually Offers

Low Offers by Design

A traditional pawn shop is a generalist business. Its staff are not trained luxury watch specialists or certified gemologists, and its business model depends on wide margins between what it pays and what it resells. The result is predictable: offers that rarely exceed 20–30% of an asset’s true market value, regardless of the piece’s brand, rarity, or secondary market demand.

The Risk of Mispricing Your Asset

When a pawn shop appraiser does not recognize the significance of a full-set Rolex Daytona or a GIA-certified diamond, the offer reflects that ignorance — not the asset’s value. A Patek Philippe Nautilus and a generic Swiss watch may receive offers of similar magnitude simply because the appraiser cannot differentiate them. For owners of genuinely valuable pieces, this mispricing is not just inconvenient. It is costly.

How a Specialist Lender Is Different

Expertise That Changes the Offer

A specialist luxury asset lender like Vasco Assets employs certified professionals who actively follow secondary markets for watches, diamonds, and fine jewelry. They understand the value of a discontinued reference, the premium attached to original box and papers, and the difference in market depth between a Rolex Submariner and a lesser-traded piece. That expertise translates directly into higher loan-to-value ratios for borrowers.

What “Up to 80% LTV” Actually Means in Practice

Loan-to-value ratios at specialist lenders are not marketing language — they are the result of accurate, market-informed appraisals. Vasco Assets bases loan offers on current secondary market data, not conservative wholesale assumptions. Two pieces with similar retail prices can still receive different offers depending on liquidity, brand recognition, documentation, condition, and price volatility.

The Hidden LTV Variance Problem

Why “Up to 80%” Is More Complex Than It Appears

Most comparisons between pawn shops and specialist lenders present loan-to-value as a stable range. In practice, this framing is incomplete. LTV is not a fixed bracket — it is a dynamic pricing output shaped by micro-market conditions, even when two assets appear identical on paper.

The Variables That Drive Real Offers

Two visually identical Rolex Submariners can receive materially different offers depending on factors that rarely appear in consumer-facing explanations. Those variables include dealer inventory exposure, short-term market velocity, recent service history, and case and bracelet wear that affects resale desirability. Regional arbitrage gaps between local and global secondary markets also play a role.

Institutional Frameworks Back This Up

This variability is consistent with broader collateral lending principles used in institutional finance. The Basel Committee on Banking Supervision notes that collateral valuation is inherently risk-sensitive and market-dependent, especially for assets with variable liquidity profiles. The Federal Reserve’s discount window collateral guidance similarly emphasizes that collateral must be valued with appropriate haircuts applied — rates that fluctuate with market conditions rather than remaining static.

LTV as Pricing Intelligence, Not a Fixed Promise

Understanding LTV as a fluid output of liquidity modeling — not a fixed promise — changes what “up to 80%” actually means. It reframes lending from simple comparison shopping into pricing intelligence shaped by real market dynamics. This is why choosing a lender with genuine market expertise matters far more than chasing the highest advertised headline rate.

Borrowing Against Luxury Watches

Which Watches Command the Strongest Offers

Watches from brands with deep, active secondary markets — Rolex, Patek Philippe, Audemars Piguet, Richard Mille, and A. Lange & Söhne — consistently support strong loan-to-value ratios at specialist lenders. Specific references matter too: a Rolex Daytona in steel or a Patek Philippe Nautilus 5711 will outperform a generic sports watch simply because demand for those references is well-documented and highly liquid.

Documentation Is Equity

Original box, papers, warranty cards, and service records are not just accessories to a watch — they are value. A full-set example with documentation can command meaningfully more than the same reference without it. At Vasco Assets, every element of a watch’s presentation is factored into the appraisal, ensuring that borrowers receive the full benefit of what they own.

Borrowing Against Jewelry and Diamonds

Fine and Designer Pieces as Collateral

Signed pieces from recognized maisons — Cartier, Van Cleef & Arpels, Bulgari, Tiffany & Co., and Harry Winston among them — carry collateral value well beyond their material weight. A specialist appraiser understands that brand attribution, design rarity, and secondary market depth all contribute to a piece’s lending value. High-karat diamond rings, certified loose stones, and estate jewelry with provenance all qualify for consideration at Vasco Assets.

Why Diamond Certification Matters to Your Offer

For diamond pieces and loose stones, a grading report from the Gemological Institute of America (GIA) or the American Gem Society (AGS) independently verifies the four Cs — cut, color, clarity, and carat weight. Certified stones remove appraisal uncertainty, allowing a specialist lender to price with confidence and lend more generously. A non-certified stone of equal actual quality may receive a more conservative offer simply because the lender cannot verify its characteristics without independent documentation.

The True Cost of Choosing the Wrong Lender

What You Leave on the Table

Consider a Rolex Submariner with box and papers, currently trading on the secondary market for $12,000. A traditional pawn shop offering 25% of market value would advance $3,000. A specialist lender offering 70% of the same assessed value would advance $8,400. On a single asset, the difference in borrowing power is $5,400.

The Cost Compounds Across a Collection

For a collection of watches and jewelry, the gap widens considerably — and the cost of undervaluation compounds with every piece. Many lenders, including pawn shops, advertise no credit checks. What they cannot advertise is specialist knowledge, certified appraisals, or loan-to-value ratios that reflect genuine market pricing.

Accurate Representation Matters

The FTC’s Jewelry Guides underscore the importance of accurate representation of jewelry quality and value — a standard that specialist lenders are far better equipped to meet than generalists. Choosing the right lender is not just about speed or convenience. It is about ensuring your assets are correctly understood and fairly valued.

Some Pieces Are Too Valuable for a Pawn Shop

Know What You Own Before You Walk Through a Door

Fine watches and jewelry represent years of acquisition, taste, and financial commitment. Before accepting a fraction of their value from a generalist lender, take the time to have them assessed by someone who actually understands the market. Vasco Assets provides complimentary valuations with no obligation — and the difference between their offer and a pawn shop’s may be the most important number you discover this year.

The Right Offer Is One Conversation Away

Whether you own a single timepiece or a collection of signed jewelry, there is real capital in what you hold — and a specialist lender will see it. Request your free valuation at vascoassets.com and find out exactly what your assets can do for you, on your timeline, without giving anything up permanently.

FAQs

1. Why should I use a specialist lender instead of a pawn shop?

Pawn shops are generalist businesses that typically offer 20–30% of an asset’s true market value. A specialist lender like Vasco Assets employs certified appraisers with active knowledge of luxury watch and jewelry secondary markets, enabling loan offers of up to 80% of assessed value. The difference in borrowing power on a single high-value asset can amount to thousands of dollars.

2. Why do two similar watches or jewelry pieces sometimes receive different loan offers?

LTV is not a fixed number — it is a dynamic output shaped by factors including dealer inventory exposure, short-term market velocity, condition, documentation, and regional pricing differences. As recognized by frameworks like those of the Basel Committee on Banking Supervision, collateral valuation is inherently risk-sensitive and market-dependent. Two identical-looking pieces can receive different offers based on micro-market conditions at the time of appraisal.

3. Do I need a credit check or income verification?

No. Collateral loans are secured by the asset itself, not by your credit profile. Neither your credit score, income history, nor debt-to-income ratio are factors in the approval process — making this an especially practical option for business owners and individuals with complex financial profiles.

4. How is my asset stored and protected during the loan?

All assets are held in secure, monitored vaults at Vasco’s Newport Beach headquarters and insured by Lloyd’s and Partners of London for twice the loan amount. Your piece is fully protected and returned in the same condition upon full repayment of the principal and fees.

5. How quickly can I receive funds?

Vasco Assets can typically complete an appraisal and fund a loan within 24 hours of receiving and evaluating the asset — significantly faster than conventional financing and with far greater accuracy than a standard pawn shop assessment.

6. What are the loan terms and interest rates?

Loan terms run 30, 60, 90, or 120 days, with extensions available. Interest rates range from 2% to 10% with an average of around 5%, set in compliance with California’s Department of Justice regulations. The minimum loan amount is $2,500.

7. Can I borrow against multiple pieces at once?

Yes. Vasco Assets is experienced in portfolio-level lending and can evaluate watches, jewelry, and other luxury assets simultaneously. A combined appraisal across multiple pieces may allow you to access a larger loan than any single item would support on its own.